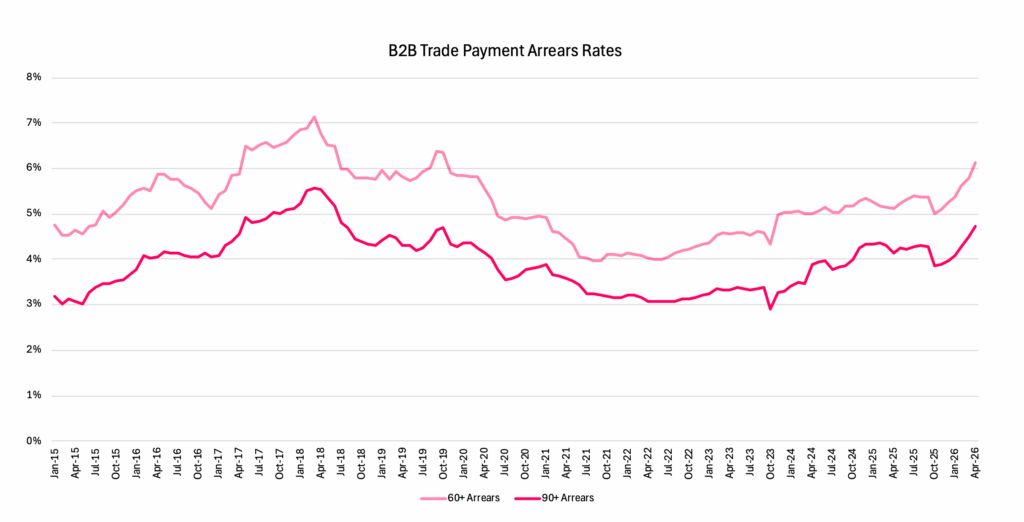

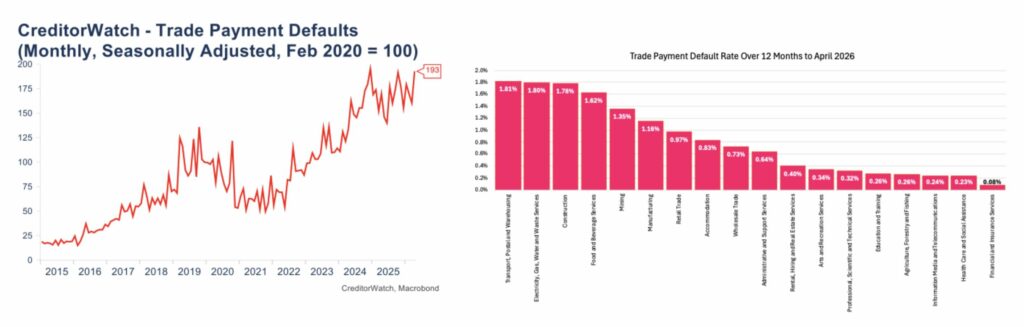

- Late payments are at a six-year high, signalling cash-flow stress is spreading across Australian businesses. A key forward indicator for insolvencies.

- Financial stress is emerging earlier in the cycle, with deteriorating payment behaviour pointing to structural vulnerabilities rather than a typical cyclical slowdown.

- A three-way squeeze is intensifying business risk: higher interest rates are lifting debt‑servicing costs, inflation and energy prices are pushing up operating expenses and weak demand is limiting businesses’ ability to pass on costs.

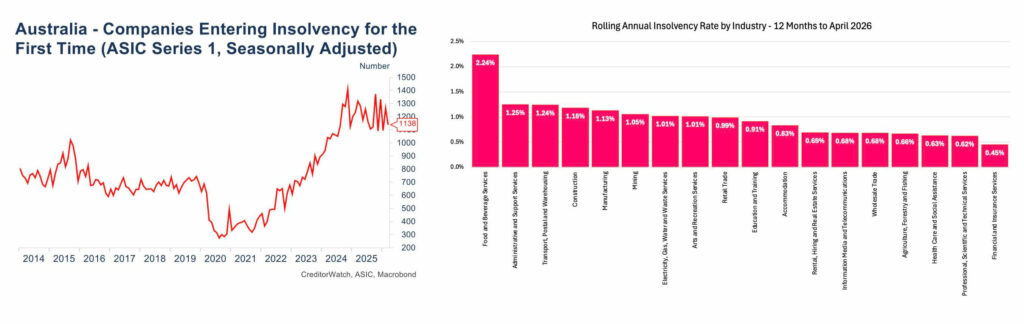

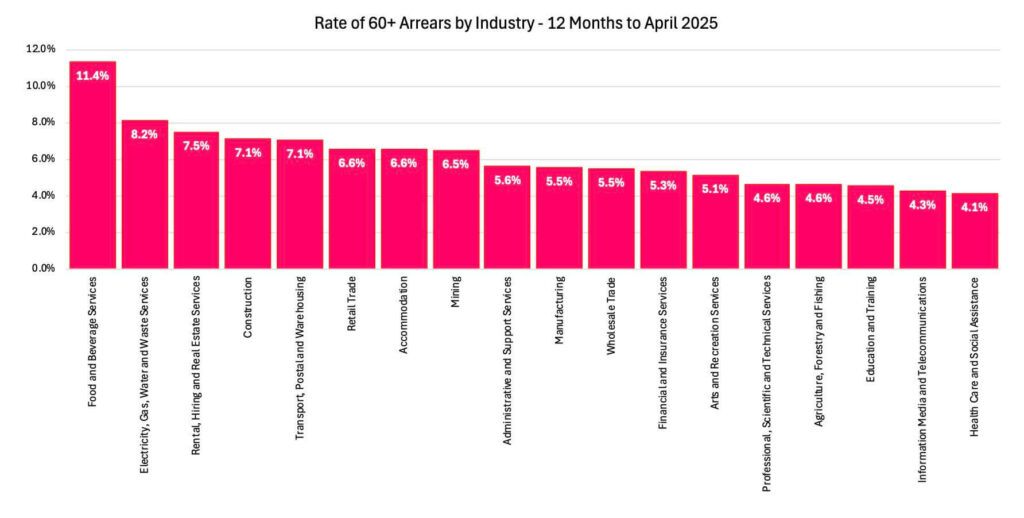

- Pressure is uneven across the economy, with hospitality, construction, transport, manufacturing and other cost and demand-sensitive sectors showing the highest rates of insolvencies, late payments and invoice defaults.

- Global uncertainty is compounding domestic pressures, as impacts from the Middle-East conflict feed through to higher fuel costs and inflation, further tightening margins and cash flow for Australian businesses.

The April Business Risk Index results from CreditorWatch show Australian businesses are being hit by a three-way squeeze: inflation and energy costs are lifting operating expenses, higher interest rates are tightening credit and debt-servicing capacity, and weak consumer demand is limiting the ability to pass costs on.

CreditorWatch data reveals financial stress is appearing earlier in the cycle as more businesses struggle to pay their invoices on time – a strong indicator of structural vulnerabilities in the system rather than a normal cyclical downturn.

This deterioration in payment behaviour is a key early warning sign for future insolvencies. The April Business Risk Index results show that the pressure building across the economy is now showing up in the invoice ledger.

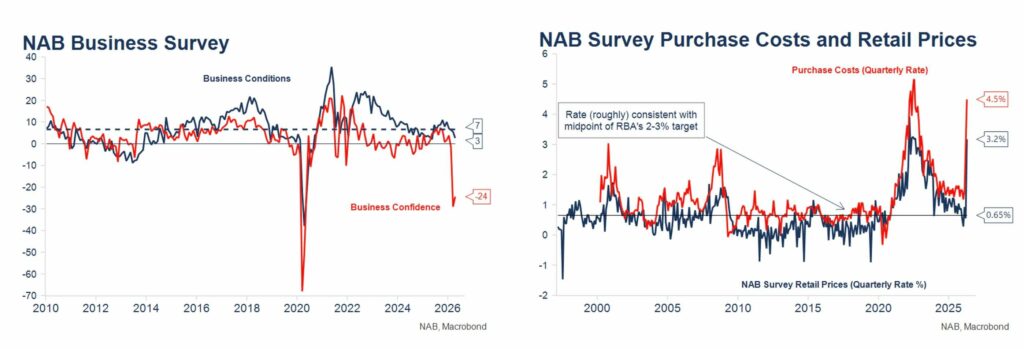

The macro backdrop explains why the increase in the arrears rate is an ominous sign for Australian business conditions. The Reserve Bank of Australia’s May Statement on Monetary Policy says inflation remains above target, higher fuel prices are adding to inflation and there are signs these costs are likely to have second-round effects on broader goods and services prices.

The RBA increased the cash rate target by 25 basis points to 4.35 %, assessing that inflation is likely to remain above target for some time. It noted in its summary that higher fuel prices and this year’s interest rate increases are expected to lower spending by Australian households and businesses.

That combination matters for business risk. Higher rates lift debt-servicing costs. Higher energy and transport costs squeeze margins. Softer demand makes it harder to pass on costs. The result is a more fragile cash-flow environment, especially for smaller operators and sectors with tight margins.

The near-term outlook remains heavily influenced by Middle East developments, oil prices and inflation pressure, with input costs rising sharply due to fuel and broader energy impacts.

CreditorWatch CEO Patrick Coghlan says, “the April data shows the business risk story has moved from macro pressure to measurable cash-flow behaviour. We are not seeing a sudden collapse in business conditions, but we are seeing a less forgiving trading environment. More invoices are sliding beyond 60 days overdue, and the stress is concentrated in sectors central to household spending, supply chains and small business employment.

“Businesses extending credit should be watching customers more closely, acting earlier and using live risk signals rather than waiting for problems to become visible in arrears or payment defaults.”

CreditorWatch Chief Economist Ivan Colhoun says, Australian economic data to date shows only a slight deterioration in business conditions, but much bigger impacts on confidence and input costs.

“The surge in input costs and retail prices add to prior cost of living and cost of doing business pressures and can be expected to lead to weaker business conditions in coming months unless the Strait of Hormuz reopens relatively soon,” he says. “The third successive interest rate increase by the RBA to address Australia’s pre-existing above-target inflation will add additional pressure to businesses and consumers in coming months.”

The Middle-East conflict is still a relatively recent development for business and the economy. As such, developments in the economy are likely to be evolving well ahead of the official economic data. The same is likely to be true of some of the traditional credit and insolvency indicators we report on.

To detect emerging trends in credit as early as possible, we have been monitoring the daily data for both credit enquiries and B2B trade payment defaults. The data suggests there has been a mild increase in concern, reflected in modestly higher volumes of credit enquiries. Similarly, the number of invoice defaults registered on the CreditorWatch platform has also lifted moderately, though the value of defaults has risen a little more significantly, likely reflecting some greater credit concern.

Where the pressure is biting hardest

The sector data shows the pressure is uneven. Food and Beverage Services recorded the highest rolling annual insolvency rate at 2.24%, followed by Administrative and Support Services at 1.25%, Transport, Postal and Warehousing at 1.24%, Construction at 1.18% and Manufacturing at 1.13%. These are sectors exposed to discretionary spending, labour costs, fuel, materials, subcontractor risk and supply-chain disruption.

The late-payment picture reinforces that sector split. Food and Beverage Services had the highest rate of invoices more than 60 days overdue at 11.37%, followed by Electricity, Gas, Water and Waste Services at 8.16 %, Rental, Hiring and Real Estate Services at 7.51%, Construction at 7.15%, Transport, Postal and Warehousing at 7.09% and Retail Trade at 6.59%.

The industries that have seen the largest increases in payment defaults have been Retail, Food and beverage Services (Hospitality), Wholesale Trade, Transport, Postal and Warehousing, and Finance and Insurance Services. This reflects their relatively greater exposure to both interest rates and energy prices, though both have impacted quite broadly throughout the economy.

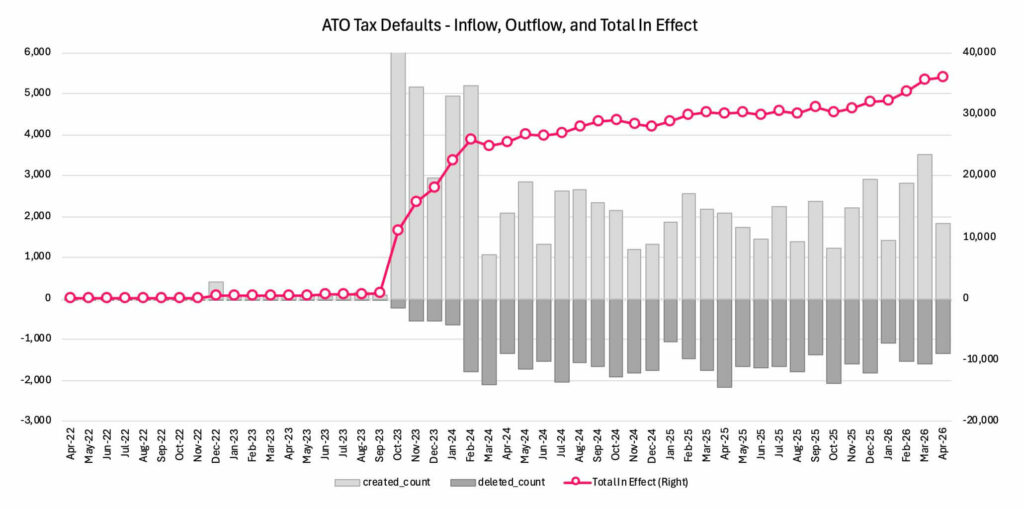

ATO tax debt defaults rising

CreditorWatch’s ATO default data for April shows an increasing number of businesses are falling behind on their tax payments. Three of the four highest new inflows since the increase in enforcement post COVID, have been recorded in the past four months. There is a considerably higher risk of insolvency over the coming 12-month period, for companies carrying large ATO debts.

Tax-debt pressure remains heavily concentrated among smaller and less-structured business entities. Sole traders account for 54% of outstanding tax debt defaults greater than $100,000.

Sole traders and smaller operators typically have less separation between business cash flow and personal finances, fewer capital buffers and less capacity to absorb higher debt-servicing costs, energy costs or slower customer payments.

The broader context is that ATO debt has become a much larger small business stress point. The ABC reported that calls to the Small Business Debt Helpline increased 21% in the 12 months to 31 December 2025.

Middle-East conflicting compounding cash flow stress

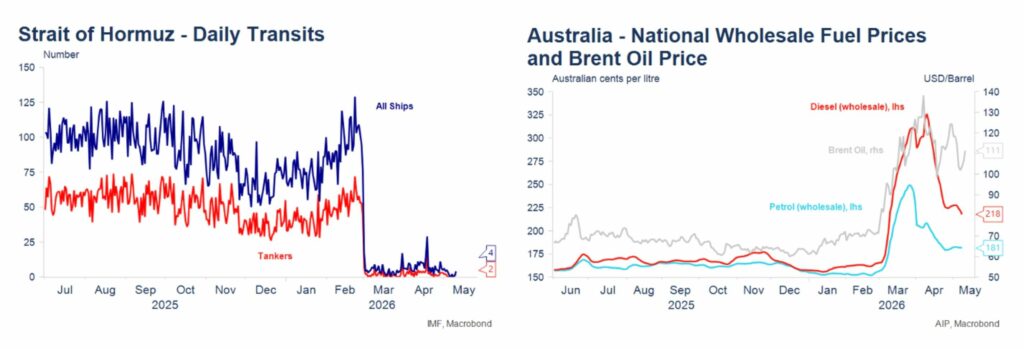

It is now two and a half months since the Middle East conflict began. The Strait of Hormuz remains effectively closed. Oil prices are trading around US$100 per barrel – about 20% below their recent highs as markets remain hopeful that a peace deal may be reached as negotiations continue between the US and Iran.

The longer the Strait of Hormuz remains closed, the greater the risk of a renewed very sharp spike in energy prices and interruptions to energy supplies as emergency global stocks cannot be rundown indefinitely. Australian petrol and diesel prices have fallen back from their highs. Prices would be over 30 cents per litre higher without the temporary cuts to fuel excise tax and road user charges by Australian governments, which are due to expire at the end of June.

The outlook

CreditorWatch Chief Economist Ivan Colhoun says, interest rates and energy prices have been adverse for businesses in recent months and are important macro drivers of insolvency.

“This is evident in the recent sharp drop in CreditorWatch’s Economic Conditions Tracker. Higher energy costs are a significant part of the deterioration in the indicator. These prices could reverse relatively quickly if a peace agreement is signed soon, but by the same token, energy prices might rise sharply further were the Strait of Hormuz to remain closed for an extended period.

“This uncertainty is of course very difficult for businesses. Encouragingly, the outlook for the Australian economy seemed to be improving ahead of the Iran conflict, though recent interest rate rises will no doubt be a headwind across the second half of the year. If an agreement to reopen the Strait can be reached soon, there is a reasonable prospect that these more favourable economic conditions can be re-established. Parts of the mining sector are performing strongly and the WA economy seems to be benefiting from the continuing AI investment boom and global data centre rollout.”

Want to know more?

To learn more about how we can help you improve your cash flow management process, get in touch with our friendly team at CreditorWatch today.

Frequently Asked Questions

What are business conditions in Australia like at the moment?

What is driving the sharp increase in late payments and arrears?

Which industries are under the most pressure right now?

Why is rising ATO tax debt a growing concern for business risk?

Get started with CreditorWatch today

Take your debtor management to the next level with a 14-day free trial.