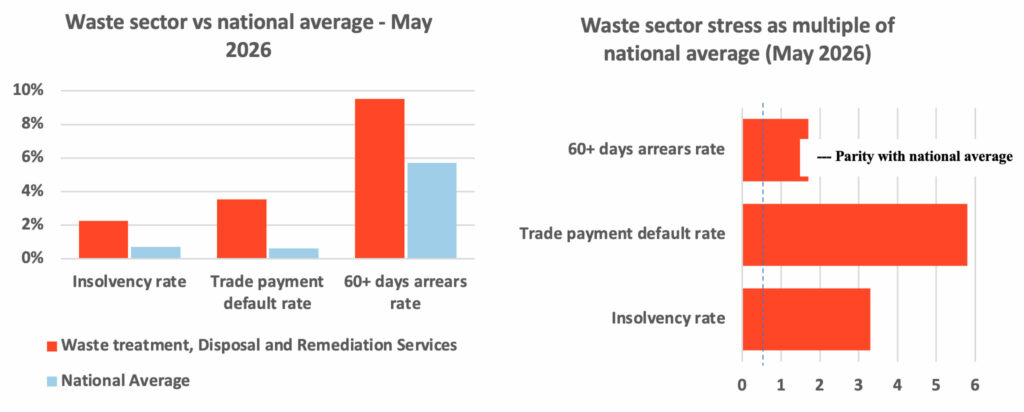

- Waste sector stress hits new extremes – insolvencies are at a two-year high and running at more than 3x the national average, with arrears near record peaks.

- A defensive sector turned distressed – once a steady performer, waste services appear to have decoupled from the broader economy since the pandemic.

- A ‘pressure stack’ is squeezing operators – fuel, interest rates, landfill levies, compliance costs and construction exposure are hitting margins, cash flow and balance sheets all at once.

- Policy headwinds will blunt the oil-price relief – three RBA hikes and a 4.75% award wage rise from 1 July will keep pressure on businesses, even as the oil price normalises.

- Headline calm expected to give way to building pressure – May insolvencies hit a two-year low, but payment defaults spiked and ATO tax defaults have been rising.

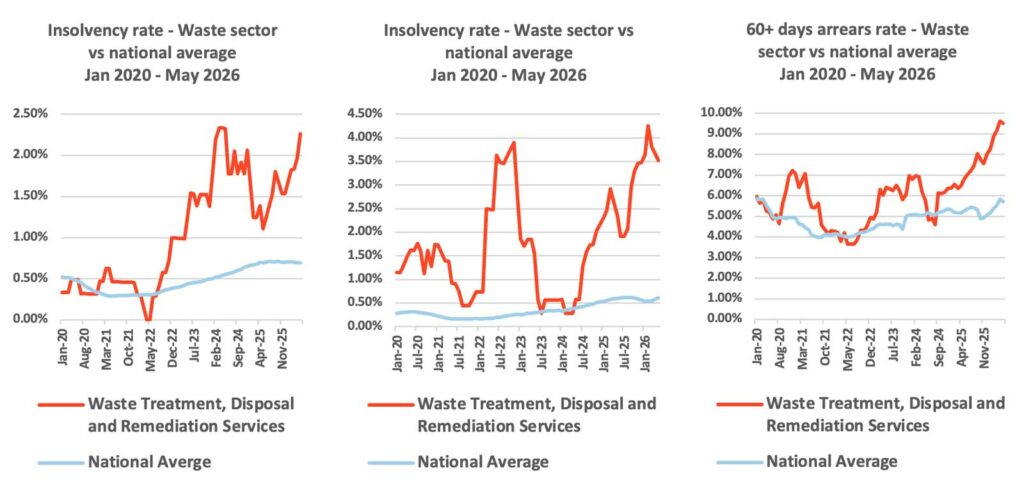

CreditorWatch’s May Business Risk Index results show pressure continuing to intensify in the Australian waste services sector with insolvencies at their highest level in two years and payment defaults and 60+ day arrears near record highs.

This combination is particularly significant. Insolvency data, by its nature, lags the cycle. Payment defaults and arrears, by contrast, are forward-looking indicators. When all three are elevated simultaneously – especially when defaults and arrears are near historical extremes – it points to a system under acute strain

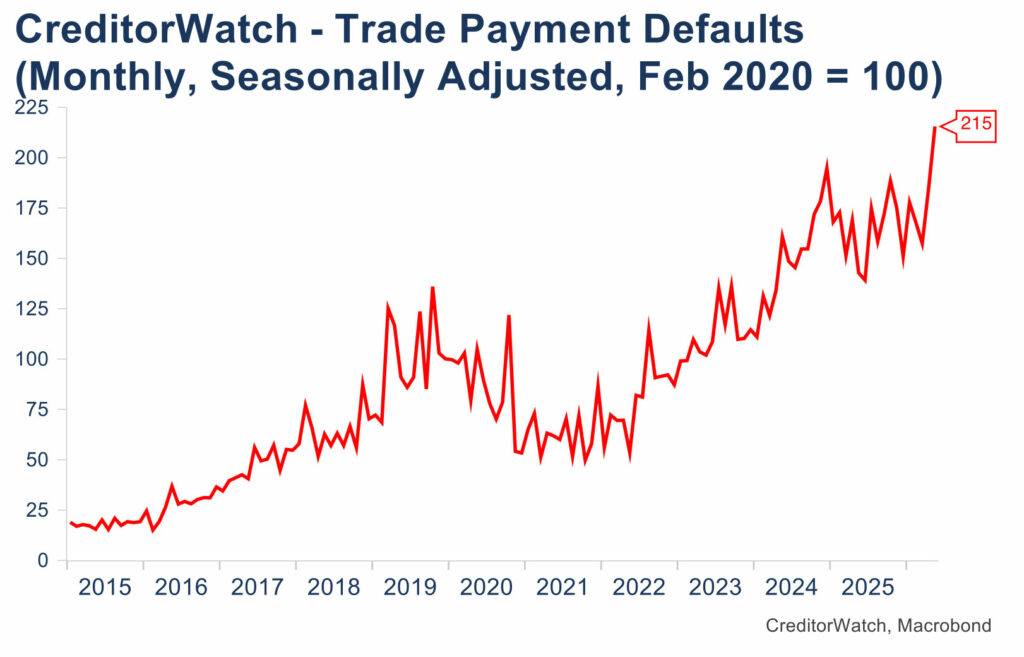

The data makes that clear. Insolvencies in the sector are running at more than three times the national average, while trade payment default rates have recently dropped to 3.5% from a record high 4.3% in February. This compares to a current national average for all sectors of 0.6%.

At the same time, 60+ day arrears have climbed back to levels close to their historical peak, indicating that payment behaviour across the sector is deteriorating broadly, not just among the weakest firms.

CreditorWatch CEO Patrick Coghlan says, “What we’re seeing in waste services is one of the clearest signals yet that credit risk in Australia is becoming more concentrated, more fast-moving and more behavioural.

“The businesses that will navigate this environment best are the ones that can spot stress early – in payment behaviour, arrears and changing trading patterns – and act before those pressures turn into serious financial distress. That is why real-time risk intelligence is now essential for protecting cash flow, managing exposure and making confident decisions in a tougher economy.”

From defensive to stressed: a major shift in the sector

For much of the past decade, waste services were regarded as a defensive part of the economy. Demand was stable, underpinned by households, local government and construction activity. Insolvency rates were relatively low and, at times, below the national average.

That has changed decisively since the pandemic. A sector that once benefited from predictable demand is now operating under a set of cost and policy conditions that are both more volatile and more difficult to pass through.

This is most clearly seen in the widening gap between the waste sector and the rest of the economy. As recently as 2020, insolvency rates in the sector were lower than the national average. By May 2026, they were more than three times higher. Trade payment defaults and arrears show a similar divergence.

This widening gap is important. It signals that the pressures affecting the broader economy – higher interest rates, rising input costs, slower demand – are not being felt evenly. Instead, they are being concentrated in specific sectors with particular structural characteristics. Waste services is one of the clearest examples.

The pressure stack: multiple shocks, one outcome

The waste sector is currently experiencing a combination of interacting forces compressing margins, disrupting cash flow and weakening balance sheets.

At the most immediate level, the 2026 energy shock has had a direct and measurable impact. Waste collection is highly transport-intensive, and diesel represents a significant share of operating costs. When fuel prices rise sharply, those costs feed straight into the business. Unlike many other industries, however, waste operators often cannot pass those increases on quickly. Contracts with councils and commercial clients are typically fixed or indexed to CPI, not to fuel costs, meaning that operators absorb the shock in real time.

On top of this is the continued rise in landfill levies. These charges are deliberately set to discourage landfill use, but their impact varies significantly across the sector. Sydney, for example, is rapidly running out of space for landfill.

Large, vertically integrated operators with their own landfill and recycling infrastructure are better positioned to manage or offset these costs. Smaller operators – which make up a substantial share of the industry – face a far more direct hit to margins, with limited ability to recover the increase.

The compliance landscape has also shifted. Changes to PFAS standards, hazardous waste handling requirements and environmental enforcement have raised compliance costs across the industry. They involve more monitoring, more reporting, and higher operational thresholds, all of which increase the cost base at a time when costs are already under pressure.

At the same time, the sector remains deeply tied to construction and public sector activity. Higher construction insolvencies over the past two years have had a direct flow-on effect, with waste contractors left exposed when projects are delayed or counterparties fail. Government work, while more stable, brings its own challenge in the form of long payment cycles, contributing to working capital pressure.

Finally, there is the financing environment. Waste services is a capital-intensive industry, requiring ongoing investment in trucks, transfer stations, treatment facilities and landfill infrastructure. Higher interest rates are therefore particularly impactful, increasing debt servicing costs and making refinancing more difficult, especially for smaller operators.

How stress is showing up in the data

Taken together, these pressures have translated into a familiar but powerful set of financial dynamics for waste services operators. The first is a margin squeeze. Costs – fuel, labour, compliance, levies – have been rising faster than revenues, eroding profitability.

The second is a working capital shock. Cash outflows have accelerated, particularly for fuel and disposal costs, while inflows have remained tied to slower payment cycles. The third is balance sheet stress. As margins shrink and cash flow tightens, debt servicing has become more difficult, particularly in a higher-rate environment.

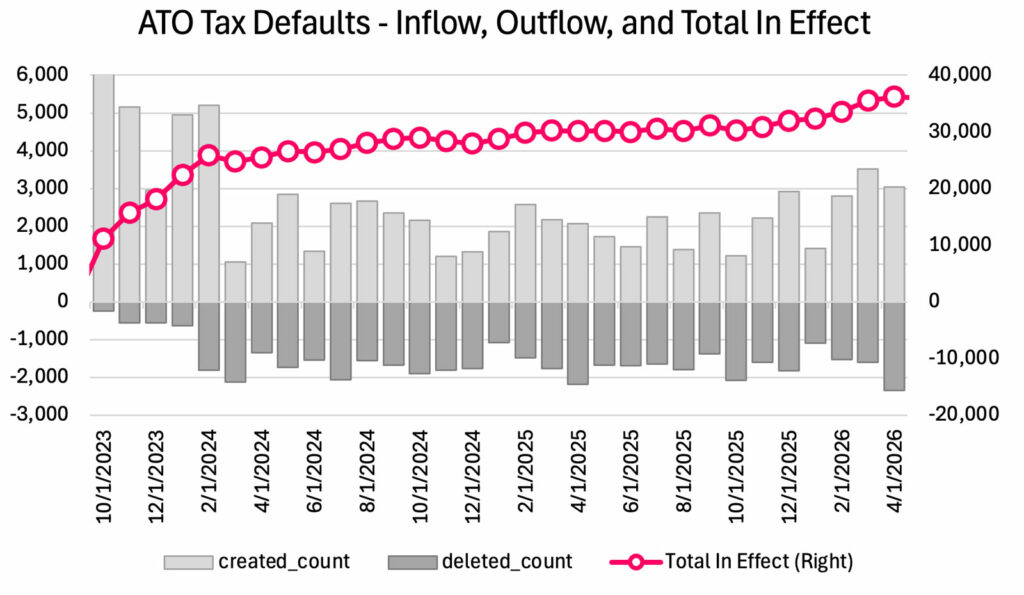

What is striking in the current data is that all three dynamics are occurring simultaneously and persistently. This is why arrears are near record highs, why trade payment defaults surged so sharply in 2025 and early 2026, and why insolvencies are now rising again from an already elevated base.

In a typical cycle, these indicators move sequentially – arrears first, then defaults, then insolvencies. In the waste sector, they are overlapping. That overlap is the clearest signal that stress is embedded, rather than transitory.

A national pattern, not a local anomaly

While some of the most visible examples of these pressures – such as landfill constraints and levy settings – play out strongly in New South Wales, the underlying drivers are not confined to a single market.

Fuel costs, regulatory tightening, construction exposure and financing conditions are all national in scope. The same structural characteristics that make the sector vulnerable in Sydney apply across other states and regions. As a result, the waste sector’s performance should be understood as part of a broader national pattern of concentrated business stress.

This matters for the broader Business Risk Index narrative. Headline insolvency numbers at the national level may appear relatively stable, but they mask significant divergence beneath the surface. Risk is increasingly concentrated in sectors with particular structures – and waste services is one of the clearest examples.

Macro update: Oil relief in sight, but business pressure persists

Despite the parlous state of the US/Iran negotiations at the moment, an end point does seem to be in sight. In time, this should reverse a significant amount of the related inflationary pulse and supply disruptions as oil markets normalise in coming months. Businesses will still have to cope with the impacts of the three interest rate increases by the RBA and from 1 July, the unhelpfully large 4.75% modern award pay increase awarded by the Fair Work Commission.

The decision to award a large increase on a forecast of inflation, which now most likely will not be achieved due to the more recent sharp reversal in oil prices, was not good policy. It will make the RBA’s job of returning inflation to the 2.5% target harder and may result in an otherwise unnecessary further increase in the official cash rate – both factors that will result in higher insolvencies than otherwise would be the case.

US longer-term interest rates are also increasing again as the new Fed Chair signals a tougher stance against inflation, which has missed targets for five years (the same is true in Australia). Longer-term US interest rates have an important influence on the three to five year borrowing rates for many Australian businesses.

Recent insolvency trends

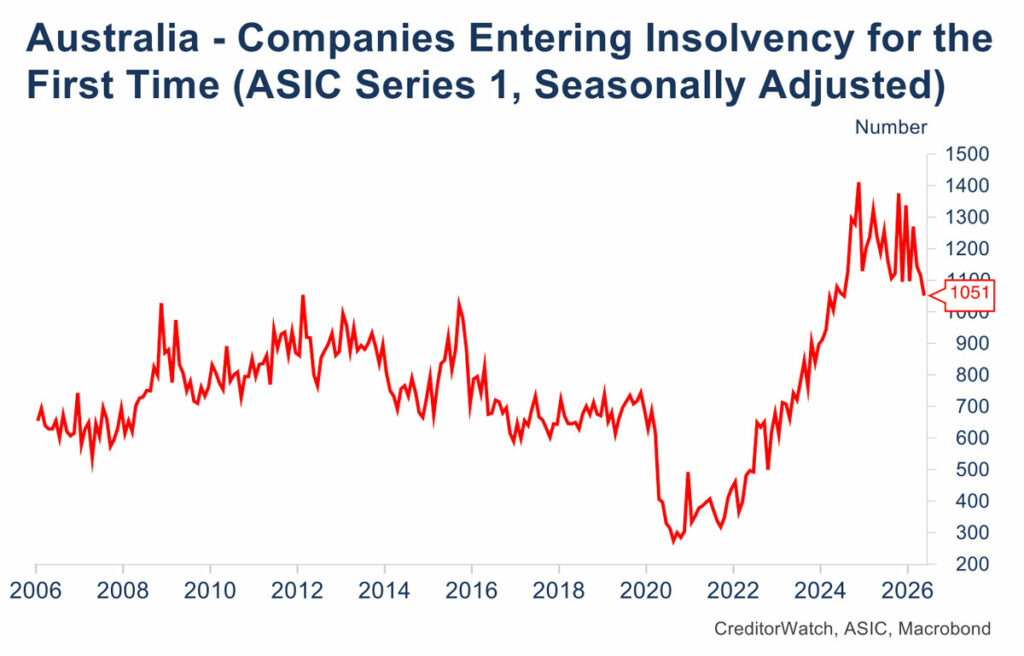

ASIC reported 1,051 first time insolvencies in May 2026, the lowest figure in nearly two years (since July 2024). Given the data can be somewhat volatile month by month, we continue to conclude that insolvencies have been broadly tracking sideways for much of the past eighteen months.

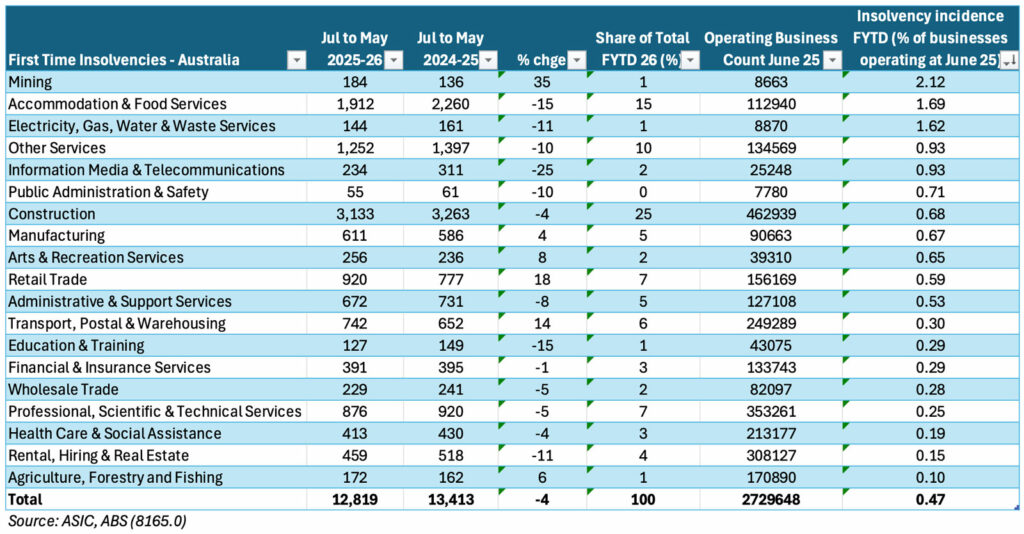

The table shows the trends in insolvencies across the different ANZSIC categories over the first eleven months of the financial year, both in absolute terms, but also ranked as a share of the number of companies operating at the end of the previous financial year. This scales the number of insolvencies more appropriately. The most notable trends are:

- Total insolvencies are around 4% lower for the first 11 months of this financial year than last, with insolvencies lower in 13 of 19 sectors.

- The overall drop is mainly due to improvements in three sectors, with relatively large absolute numbers of insolvencies: Accommodation & Food Services; Construction; and Other Services. In each case, the rate of insolvency for these sectors is higher than the average rate of insolvency of just under 0.5% of companies.

- Two sectors in particular, have had higher incidence of insolvency than last year – Retail Trade and Transport, Postal & Warehousing.

Warning lights flash: Payment and tax defaults signal rising insolvency risk

Two of the key pieces of information that we use as reliable leading indicators of potential insolvency are Trade Payment Defaults (B2B invoice defaults registered on CreditorWatch systems) and ATO tax defaults (firms with tax debts of over $100,000 to the Australian Tax Office).

Payment defaults jumped sharply in May, perhaps reflecting pressures from higher energy prices. Realistically, it’s too early for the two interest rate rises implemented before May to have had a major impact as yet. Payment defaults have remained stable across most industries and are really only recording a rising trend in Transport, Postal and Warehousing and in Retail.

The outlook

Previous CreditorWatch research has identified interest rates and energy prices as important explanators of insolvency rates. In practice, these variables likely reflect the important costs of doing business. The rise in insolvencies after the COVID dip was attributed to much higher inflation and costs along with the significant tightening of monetary policy that occurred from 2022-2024. The levelling off of insolvencies from late 2024 we attribute to both the income tax cuts of 1 July 2024 and the three interest rate cuts of 2025.

Looking ahead, there are mixed pressures. A likely normalisation in oil prices following the peace agreement is a positive, while interest rate increases and the large minimum and award wage increases recently granted will be an increasing headwind as 2026-27 progresses, particularly for interest-sensitive and discretionary spending exposed industries.

This suggests insolvencies are more likely to trend higher in the months ahead. The AI investment boom remains a positive for parts of construction and mining, as does spending on defence and aged care.

Want to know more?

To learn more about how we can help you improve your cash flow management process, get in touch with our friendly team at CreditorWatch today.

Frequently Asked Questions

What are the key findings from the May 2026 Business Risk Index?

Why is the waste services sector under such pressure?

What do rising payment defaults and arrears signal for businesses?

Are insolvencies rising across the whole economy?

What is the outlook for Australian businesses over the coming months?

Get started with CreditorWatch today

Take your debtor management to the next level with a 14-day free trial.