Key Takeaways

- Australia’s energy shock isn’t over, and it’s now a major business risk story: CreditorWatch data shows elevated fuel and energy prices are feeding directly into business stress, compounding already tight conditions from higher interest rates and weaker demand.

- Early warning signs are flashing in the data – before insolvencies spike: Deteriorating payment behaviour and persistently high ATO tax defaults are signalling rising insolvency risk over the next 12 months, highlighting why forward-looking risk indicators matter more than headline failures.

- Sole traders are bearing the brunt of the pressure: While they make up 30% of all businesses, sole traders account for 54% of large ATO tax defaults, underscoring vulnerability at the smallest end of the economy.

- Energy costs are hitting the real economy unevenly, and fast: Diesel price spikes are flowing quickly into transport costs and consumer prices, with retail and transport sectors already showing a deteriorating insolvency trend.

- The next few months will define the outlook for business confidence: CreditorWatch’s analysis shows outcomes now hinge on whether energy prices stabilise, with risks skewed toward higher interest rates, tighter credit conditions and renewed insolvency pressure if shocks persist.

SYDNEY, Wednesday 15 April 2026 – The March Business Risk Index results from leading credit reporting agency CreditorWatch shows Australia’s energy shock is far from over, with the data suggesting business risk was already rising before March’s events in the Middle East.

Elevated energy prices, supply uncertainty and geopolitical tension are once again pushing up costs across the economy, compounding the impact of higher interest rates and weak consumer sentiment. CreditorWatch’s latest data reveals early warning signs were already emerging in payment behaviour and ATO tax defaults, even before the energy crisis. This will likely add to financial pressures for Australian businesses, with sole traders showing less resilience than other entities.

A fragile calm: what the ceasefire means for oil, inflation and interest rates

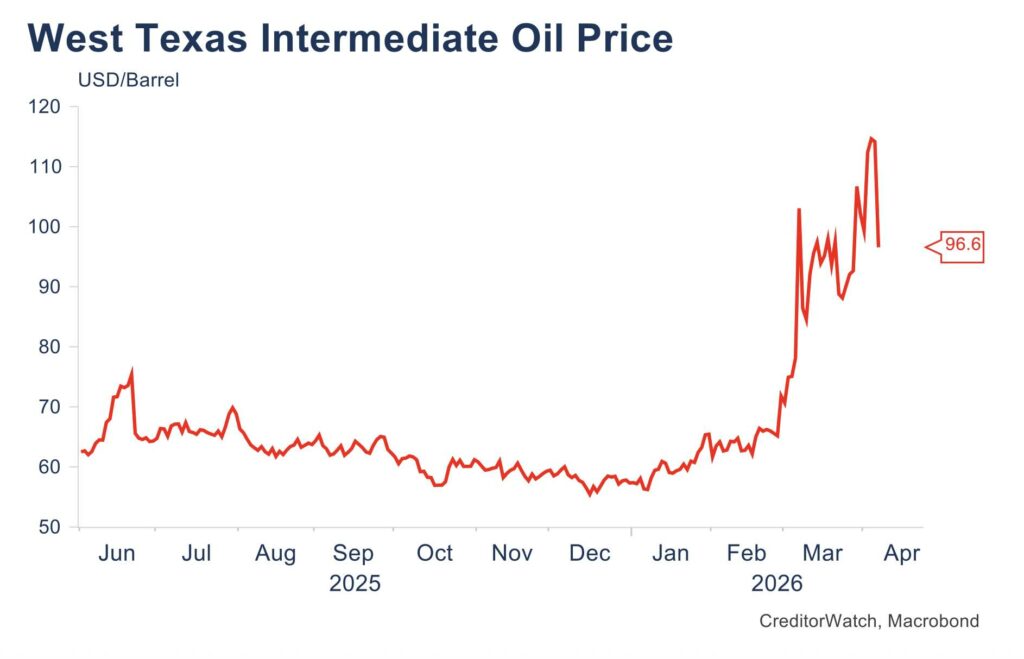

As we publish this month, a two-week ceasefire in the Middle East conflict has been agreed to, during which vessels will be permitted safe passage through the Strait of Hormuz. As the chart shows, this has brought about a partial retracement in oil prices, but prices remain much higher than the US$60-70 per barrel range that was in evidence immediately before the conflict broke out and indeed broadly throughout 2025.

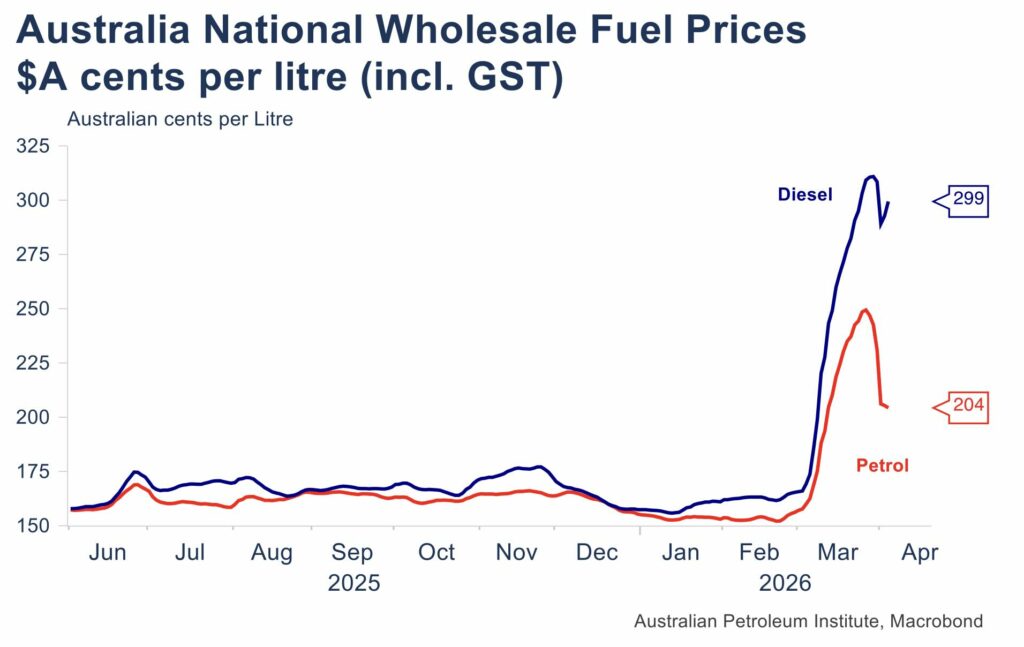

Wholesale petrol and diesel prices have experienced similar sharp rises, more so for diesel, with the slight easing in prices reflecting the combined actions of Australian governments to reduce fuel excise, heavy vehicle road user charges and refund the extra GST being collected on very high petrol prices.

The larger rise in diesel prices will produce even larger impacts for businesses, especially in energy intensive sectors, but is also flowing relatively quickly into consumer prices on account of fuel surcharges.

Possible scenarios for the Australian economy

Much of the outlook depends on the course of the military conflict and in particular: (i) in the short term, on how long the Strait of Hormuz is closed, as this removes 20% of the global supply of oil and LNG; and (ii) in the medium term, how much damage has been caused to energy-producing infrastructure in the Middle East region during the conflict.

Both of course have their impact on the economy and business not only through elevated energy prices, including also on derivative products such as fertilisers and petrochemicals used in the production of plastics, but also on supply of these products.

We can however assess two bookend scenarios, with a range of potential outcomes in between.

- Scenario 1: An early resolution to the conflict and quick re-opening of the Strait of Hormuz.

- Scenario 2: An extended military conflict and an extended closure of the Strait of Hormuz (e.g. three to six months or longer).

Australian businesses have been experiencing some aspects of the second scenario in recent weeks, with very elevated petrol and diesel prices, and in some locations, limited supply availability. However, the presence of fuel reserves likely means that the experience of the past few weeks would be milder than what would occur in the case of a very extended closure of the Strait of Hormuz. Fuel prices would need to rise sufficiently to ‘destroy’, at least temporarily, 20% of global demand. That would entail much higher prices and would likely cause a global recession, though of course, different to other recessions, the cause could effectively be reversed at short notice, if hostilities were to cease.

With the announcement of the ceasefire, Australian businesses will begin to experience the first scenario over coming weeks, with fuel prices likely to begin to drop, probably in the latter part of April and into May. Much depends on whether a more permanent plan can be inked during the two-week ceasefire, in which case it would be expected that oil and other related product prices could continue to decline as Strait of Hormuz supply is re-established.

It would not be expected that oil prices would fully retrace to pre-conflict levels immediately as it will take time to repair energy-producing infrastructure damaged in the conflict, though this is not likely to be as significant for prices as the current 20% reduction in global supply.

This should see somewhat elevated energy prices persisting for perhaps one to two further months, before the world and Australia broadly return to the economic scenario that was in prospect before the conflict broke out. That scenario included a brightening outlook for the US economy as the AI investment boom and associated global data centre rollout continued, but one likely with some additional inflationary pressures associated with very strong demand for semi-conductors, electricity, water and selected metals.

This suggests limited likelihood of further interest rate reductions globally, and instead some further interest rate rises in the months ahead, including in Australia.

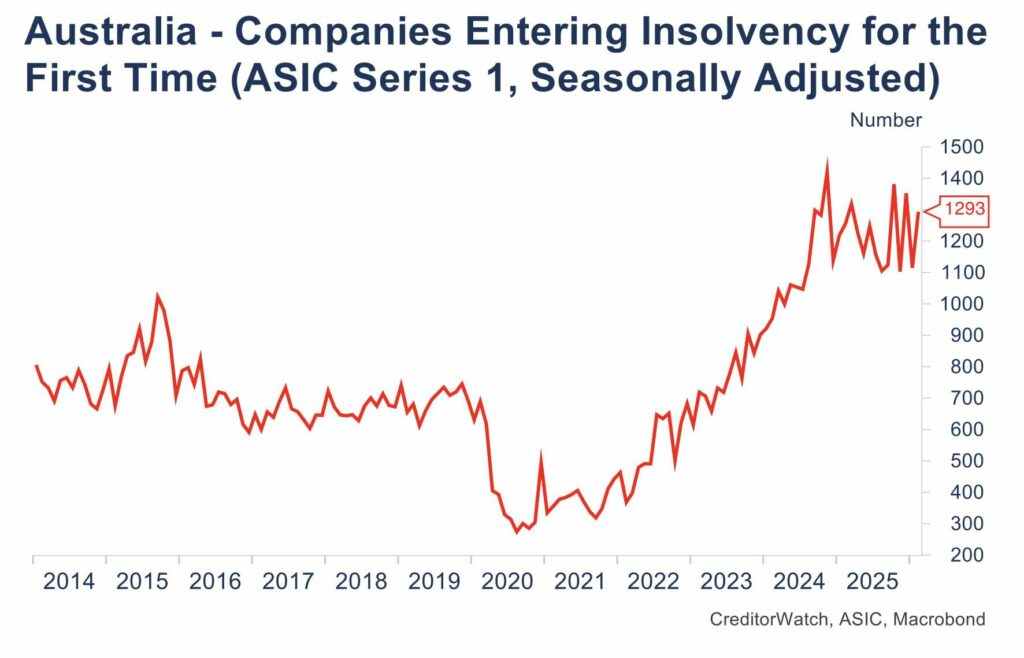

Trade payment default, ATO tax defaults and insolvency trends

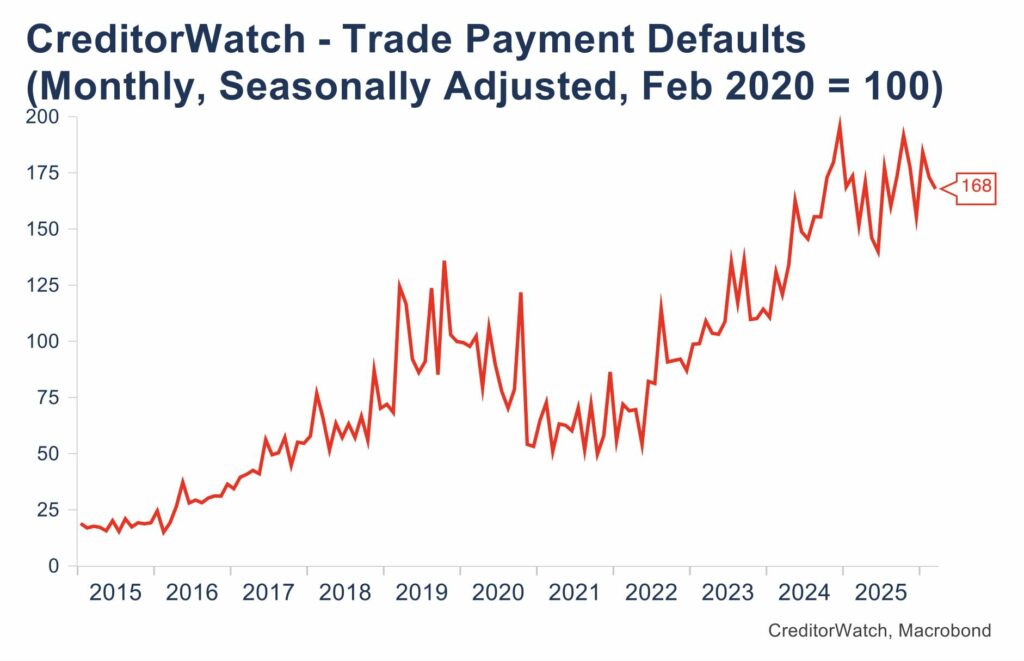

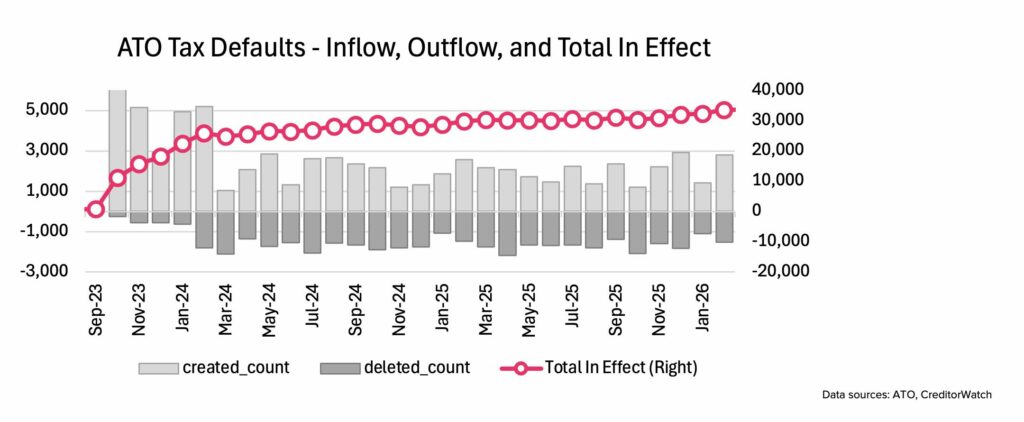

Our assessment of recent months has been that, after improving over much of 2025, the trend for our major measures of business health – trade payment defaults, ATO tax defaults and insolvencies – had begun to show some deterioration in late 2025 and the early months of 2026. This was, of course, before the events in March and the influence of the increases in Australian interest rates in February and March. This month’s data supports this assessment.

Trade payment defaults data improved slightly in the four weeks to mid-March compared to the same period in February but remain generally elevated. Like tax defaults, trade payment defaults registered against a company are a very strong predictor of potential insolvency over the next 12 months and we are expecting a renewed deteriorating trend based on recent interest rate increases along with some increased pressure from at least temporarily higher energy prices.

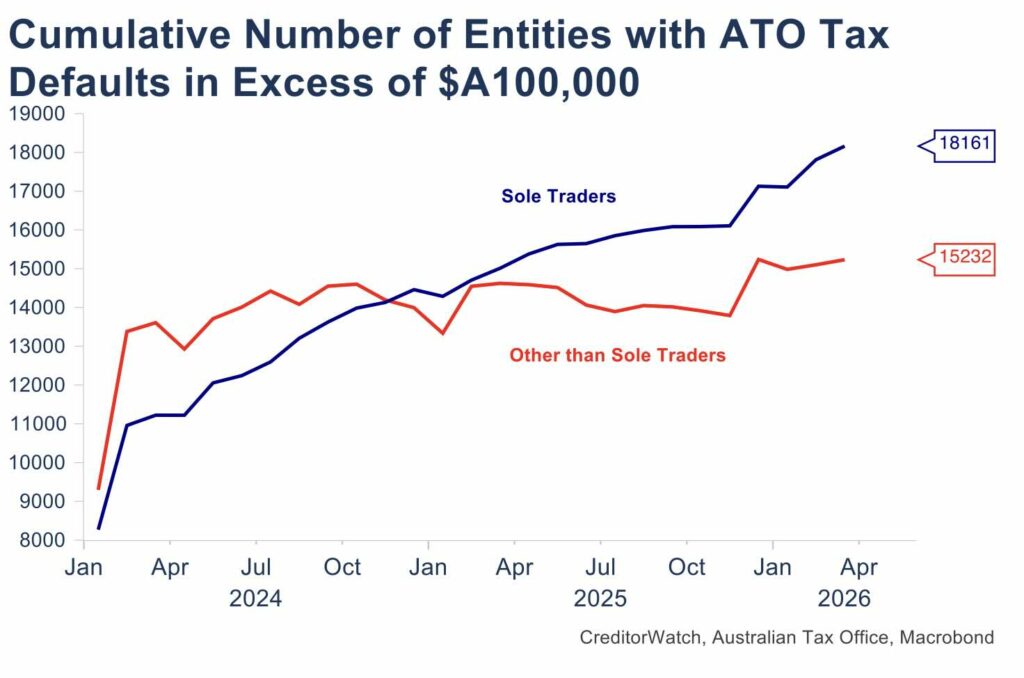

ATO tax defaults recorded another very high reading in March and four of the past six months have contained higher readings than for much of 2025. Tax defaults are a very strong predictor of potential insolvency over the coming 12 months, with recent more elevated readings suggesting a rise in insolvencies, even before recent interest rate increases.

Insolvency data has been quite volatile in recent months but presents a similar picture of elevated and possible slightly rising insolvency levels ahead of both the RBA’s actions and the energy shock in March. As in recent months, at a sector level, a deteriorating trend is evident for Retail and for Transport, Postal and Warehousing. Insolvencies have remained elevated but are no longer deteriorating in Construction and Food and Beverage Services. The increases in interest rates and energy prices are expected to create broad pressures across Australian business in coming months.

Sole traders under mounting pressure

Headline business risk remains elevated across the economy, but financial stress is becoming increasingly concentrated among Australia’s smallest businesses, particularly sole traders.

Sole traders make a significant contribution to Australia’s economy, with 822,873 single-person businesses (as at June 2025) making up 30% of all entities. However, sole traders make up 54% of businesses with a tax debt default greater than $100,000 – exceeding that of all other business structures combined.

This percentage has been growing consistently whereas ATO defaults for non-sole trader businesses have remained relatively stable.

ABS data shows the survival rate for sole-trader businesses from June 2021 to June 2025 was just 50%, compared to 68% for all companies. For sole trader businesses established in the 2021/22 financial year, just 38% were still operating in June 2025. Business-related personal insolvencies increased 52% from FY21 to FY25 according to AFSA data reflecting how business distress is transferring to household pressure for sole traders.

Across CreditorWatch metrics such as trade payment behaviour and default rates, the data points to persistent and deepening pressure at the smallest end of the market.

Sole traders typically lack the balance-sheet separation and capital buffers available to incorporated businesses, meaning tax liabilities accumulate directly against operating cash flow. As arrears persist and defaults rise, tax debt becomes both a symptom and a catalyst of deeper financial distress.

CreditorWatch CEO Patrick Coghlan says, “Small businesses are facing a much tougher operating environment than they were a year ago, and the pressure is showing in cash flow, payment defaults and tax arrears. Rising costs and higher interest rates mean even small shifts in business conditions can have outsized effects, particularly for sole traders.

“What matters is identifying those warning signs early, because once stress becomes visible at the insolvency stage, options narrow very quickly.”

The outlook

CreditorWatch Chief Economist Ivan Colhoun says, “Our previous analysis identified interest rates and energy prices as key drivers of the trend for insolvencies. Both have developed negatively in recent months, suggesting a less favourable credit environment in the months ahead.

“Hopefully, the two-week ceasefire, recently agreed to, can develop into a more lasting peace plan, because an extended conflict and closure of the Strait of Hormuz was likely to lead to much higher energy prices and supply interruptions, which would in turn set off a chain of events that would likely see the world and Australian economies end up in recession.

A relatively quick end to the hostilities and re-opening of the Strait of Hormuz should see energy prices and supplies return toward pre-conflict levels over the next few months and prevent a much bleaker outcome. That would allow pre-crisis economic fundamentals to re-establish. Those fundamentals were not completely favourable, but included:

- An improving outlook for the US economy on the back of the AI investment boom and associated data centre rollout.

- Capacity pressures associated with that rollout, including in semi-conductors, electricity, water and selected metals including copper. Capacity pressures are inflationary, suggesting limited room for further reduction in US interest rates and the likelihood that US interest rates begin to rise as the year progresses.

- Above-target inflation in Australia, requiring the RBA to enact one to two further interest rate increases in 2026.

- Parts of mining to benefit from the AI-led investment boom and elevated prices for selected commodities. This should be beneficial to the WA, QLD and NT economies in particular. Australia’s oil and gas sector could also benefit from extra demand as users seek to diversify supply sources given recent events.

Business insights

business risk index

Cash Flow

Chief Economist

Credit Management

data

defaults

hospitality

insights

insolvencies

insolvency

Interest Rates

Trump

Head of Media & Communications

Michael joined CreditorWatch in July 2021. He has more than 20 years’ experience in business journalism, marketing and communications strategy, and digital content development. He is passionate about communicating to the business community how CreditorWatch’s products can help them identify risk earlier, and make smarter decisions. He has previously written for Newscorp, Nine publishing, ACP Magazines and the World Economic Forum. He holds Bachelor of Communications and Master of Journalism degrees from the University of Technology, Sydney.

14-Day Free Trial

Get started with CreditorWatch today

Take your credit management to the next level with a 14-day free trial.