Key Takeaways

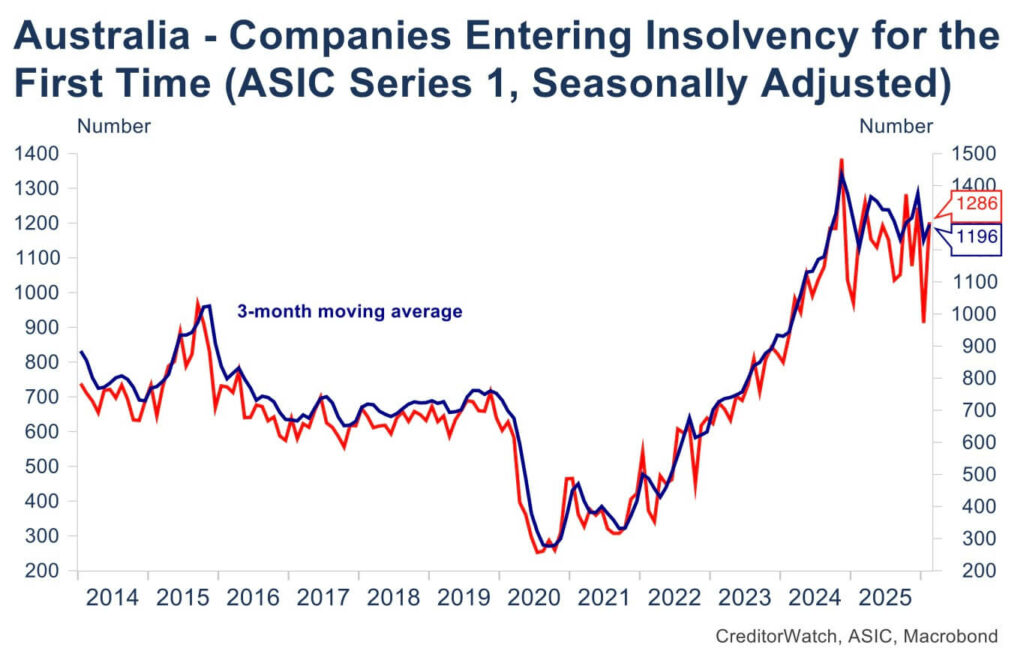

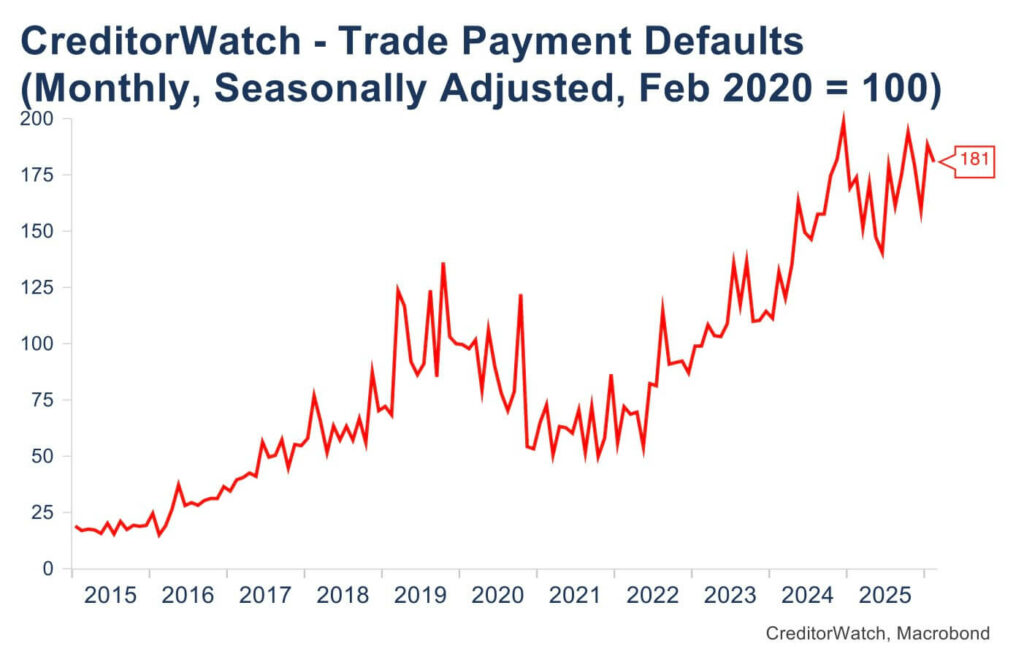

- Insolvencies are at record levels, and set to rise further – Business insolvencies and B2B payment defaults have been at or near record highs since mid 2025, with February seeing a sharp rebound in failures. With higher interest rates and an energy shock now hitting cash flow, CreditorWatch warns insolvency numbers are likely to climb again as economic growth slows.

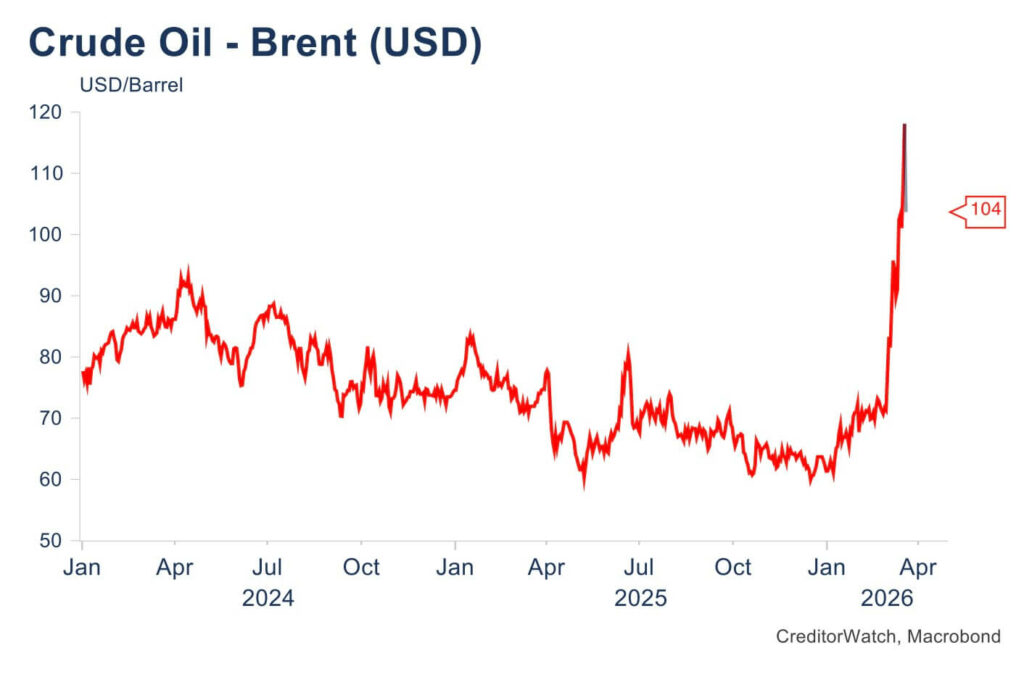

- Australia in the recession ‘risk zone’ – CreditorWatch’s Chief Economist warns that sustained oil price increases of 50-70% over six to 12 months have historically been associated with global recessions. Prices are already in that range – the critical question now is duration. If oil remains above US$125–150 per barrel for several months, recession risks rise sharply.

- Australia’s most essential sectors are now the most exposed – Industries with heavy fuel and energy use – agriculture, mining, manufacturing, construction and road transport – are facing acute cost pressures. These costs will flow rapidly through supply chains, intensifying inflation, tightening cash flow and lifting insolvency risk across the broader economy.

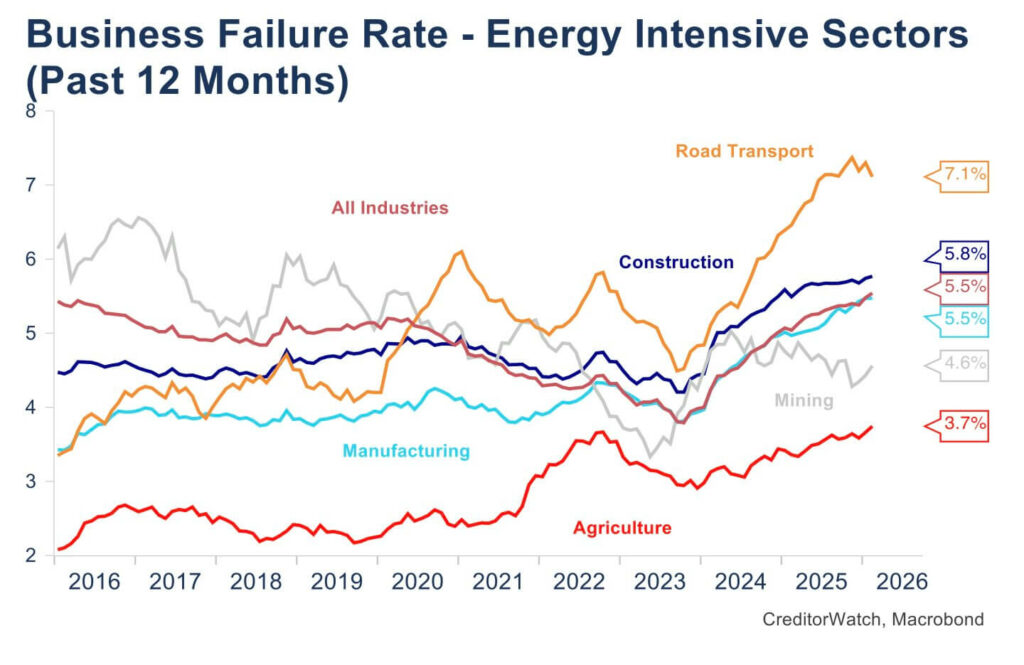

- Road transport is emerging as a critical pressure point – Fuel accounts for up to 40% of operating costs in road freight, and diesel prices jumped 36% in just two weeks. CreditorWatch data shows 7.1% of road freight businesses closed in the past year, making it one of the most stressed sectors in the economy, with flow on risks for agriculture, construction, manufacturing and retail.

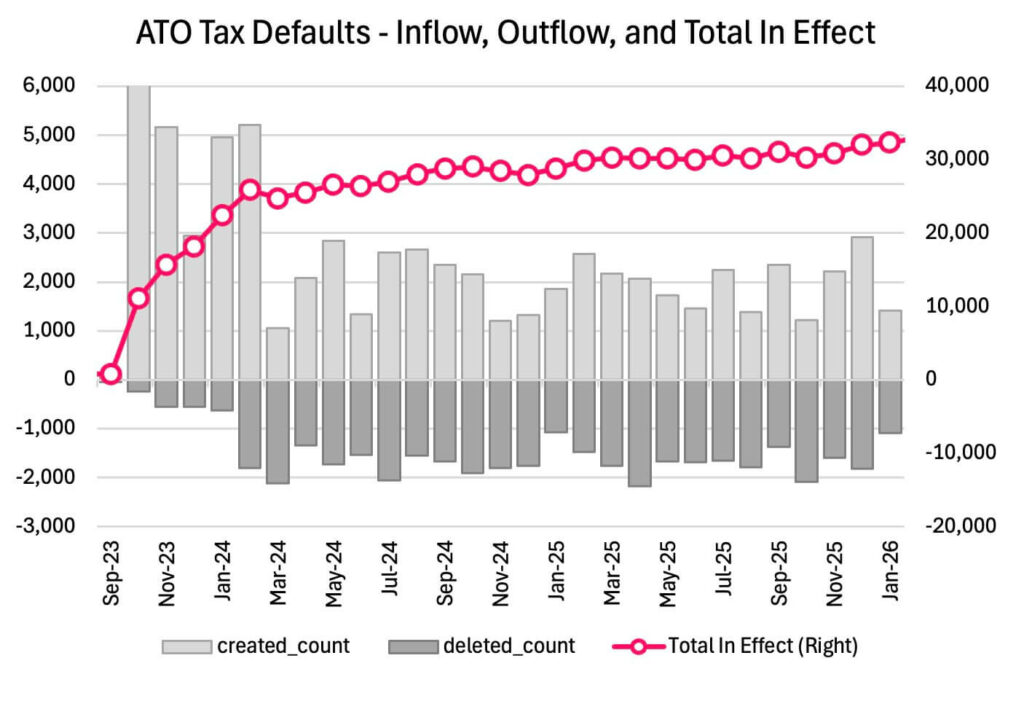

- Payment stress is flashing red before failures follow – ATO tax defaults surged late in 2025, and 60+ day payment arrears are rising across multiple sectors, including manufacturing. CreditorWatch notes these indicators typically lead insolvencies, signalling that business stress is deepening even before the full impact of the energy shock is felt.

The February Business Risk Index results from CreditorWatch reveal a troubling outlook for the Australian economy. Business insolvencies and B2B payment defaults have been at or near record highs since mid-2025, and now the conflict in the Middle East has triggered an energy price shock that is rippling through the Australian economy and threatening to push business closures even higher.

Last week’s interest rate increase – with another in May looking increasingly likely, as the RBA attempts to wrestle inflation under control – is further compounding the pressure on Australian businesses, particularly SMEs. Unless oil prices fall relatively soon – or there is government support for impacted businesses – it must be expected that there will be a rise in the number of insolvencies as economic growth slows.

The sectors with heavy fuel and power usage – agriculture, mining, manufacturing, construction, and road transport – are under acute cost pressure, straining cash flow and raising insolvency risks. They will be forced to pass on the higher costs of diesel, petrol, gas and electricity to trading partners and consumers, further exacerbating inflation, tightening cost-of-living pressures and reducing demand in the economy.

CreditorWatch CEO Patrick Coghlan says, “Australia’s small and medium sized businesses are facing one of the most challenging operating environments we’ve seen in years, with cost pressures, interest rates and global volatility all converging at once.

“The data is clearly showing that these pressures are feeding through to cash-flow stress, slower payments and a rising risk of business failure, particularly for smaller operators with limited buffers. These indicators underscore just how exposed many SMEs are to sustained economic shocks.”

Trends ahead of the fuel price shock

Ahead of the large rise in energy prices and emerging energy supply chain disruptions through March:

- Insolvencies bounced back sharply in February, which we expect to continue. The pre-oil crisis trend was a moderate decline.

- CreditorWatch’s proprietary B2B invoice defaults series is a leading indicator of the trend for insolvencies. Like the trend for insolvencies, there was some improvement evident in the first half of 2025, however registered invoice defaults deteriorated a little in the second half of the year.

- ATO tax default counts rose sharply in December, to the highest level since the significant ramp-up in collections activity that occurred post COVID, though these eased back in January (note this data is not seasonally adjusted). Like, payment defaults, this will be a very important indicator to watch in coming months.

What are the chances that the oil price will trigger a recession?

CreditorWatch Chief Economist Ivan Colhoun says there are several important considerations required to answer this question, including, how high oil prices rise, and importantly, the length of time that oil prices stay highly elevated.

Another important consideration is the potential that fuel supplies might not be available (at any price), something that there have been reports of in some regional areas of Australia. The latter is akin to the supply chain disruptions that characterised many goods during the COVID period, with fuel obviously a very central component of virtually all aspects of an economy.

Developing these themes a little more deeply, oil price rises of 50-70% that are sustained over a six to 12 month period in the past have often been associated with global recession, constituting both a very significant and importantly, sustained price shock.

The size of the oil price rises so far experienced are in that 50-70% range, however, these higher prices have only been experienced for around three weeks. The ultimate duration of higher oil prices depends on two factors: (i) the length of time the Strait of Hormuz, through which 20% of global production of crude and LNG flows daily, remains closed; and (ii) the damage inflicted on the region’s energy infrastructure during the conflict. A quick reopening of the Strait of Hormuz, would likely see oil prices drop sharply.

An extended closure, could see much, much higher oil prices, as markets would push prices up high enough to ration or ‘destroy’ an equivalent amount of demand. The latter scenario, could see fuel supplies severely disrupted causing interruptions to economic activity in a similar vein to the lockdown activity ‘disruptions’ during the COVID pandemic.

What the markets say

Markets have reacted similarly to the way they did during the 1990s Gulf War, with the oil price sharply higher, share markets falling and bond yields rising, pushing up borrowing costs. The impact on oil prices was relatively short-lived (a few months) on that occasion as the important background economic context was that the US and Australian economies were already entering recession, accentuated but not caused by oil prices.

The recession reflected a commercial property price bust, caused by overinvestment and very high interest rates. As unemployment continued to rise through H2 1990 and through 1991, central banks focused on domestic fundamentals and eased interest rates, despite temporarily higher inflation.

The domestic economic backdrop at the current time is one of very low unemployment and above-target inflation. At central bank meetings around the world last week, central bankers signalled concern about inflation more so than worries about growth and unemployment. This suggests the near-term likelihood is of some further upward pressure on interest rates, which markets are already pre-empting to a certain extent.

Sectoral impacts

Fuel crises are particularly significant economic shocks, because of the breadth of their impact across the economy and the speed with which the shock is transmitted. While the sectors with very heavy fuel and power usage – agriculture, most of mining, manufacturing, construction and road transport – are under the most acute cost pressures, higher input costs from these businesses, especially for road freight transport, flow quickly to other sectors.

Consumers also feel the costs via their consumption of energy, most noticeably at the fuel pump. One can expect to see fuel surcharges being implemented very quickly throughout the economy, adding strain to cash flow and raising insolvency risks.

They will be forced to pass on the higher costs of diesel, petrol, gas and electricity to trading partners and consumers, further exacerbating inflation, tightening cost-of-living pressures and reducing demand in the economy.

Road freight transport

The road transport sector was already experiencing some stress, before the Middle East conflict. With fuel accounting for up to 40% of operating costs, the recent surge in diesel prices – up 36% in just two weeks – has placed immediate pressure on margins. While larger operators may partially offset this through fuel surcharges, smaller firms, which dominate the sector, often lack the pricing power or contractual flexibility to do so. As a result, many may need to absorb part of the cost increases directly, leading to some cash flow deterioration.

CreditorWatch’s Business Risk Index data reveals that road freight is now one of the more stressed sectors in the Australian economy. 7.1% of businesses in the sector closed in the past year, up from 6.2% a year earlier.

Prior to the recent developments, operators were already citing a combination of rising fuel and finance/insurance costs, driver shortages, compliance pressures and intensifying competition – particularly from low-cost and foreign-backed entrants – as key challenges.

The outlook for the sector is highly contingent on the duration and severity of the oil price shock. Should the conflict de-escalate by mid-2026, fuel prices should retreat, allowing many operators to recover. However, even in this scenario, insolvency rates are expected to remain elevated through the first half of the calendar year. Conversely, if oil prices remain above US$120 per barrel for an extended period, the sector could face additional business failures, particularly among smaller and mid-sized firms. This would likely accelerate consolidation, with larger players absorbing market share, but at the cost of reduced competition and potential supply chain disruptions.

The road freight sector’s centrality to the broader economy – underpinning agriculture, construction, manufacturing and retail – means stress in this sector has implications far beyond its own balance sheets. The February BRI data highlights the sector as a critical pressure point in the current economic environment. Without targeted relief or a stabilisation in energy markets, the risk of broader disruption will continue to rise.

Manufacturing

Manufacturing in Australia covers a diverse range of businesses – from food processing to building materials, chemicals, and metals fabrication. Most subsectors are sensitive to energy prices. Many manufacturers use natural gas or electricity for heat, refrigeration or machinery, and fuel costs factor into distribution. Petrochemicals used in the production of plastics, are also impacted by the closure of the Strait of Hormuz.

The recent jump in energy prices will also have an immediate effect on input costs for manufacturing, while transport costs also rise. One very minor offset, relative to the increase in input costs is a slightly stronger Australian dollar.

Even before this conflict, Australian manufacturing was under some strain from rising input costs, partly due to the tail of the COVID pandemic and supply chain issues. The BRI data in February shows a business failure rate of 5.5% for the previous 12 months, in line with the national average. This was up from 5.0% in February 2025.

This is modest but it is rising and any upward pressure is concerning because small manufacturers in particular can become insolvent quickly if bills go unpaid. Notably, payment arrears (60+ days overdue invoices) are up 9.4% year-on-year for manufacturers, hinting at growing cash stresses even before the oil shock.

We anticipate a moderate increase in manufacturing insolvencies in the next 6-12 months. Sectors to watch are energy-intensive or trade-exposed manufacturers: e.g. makers of construction materials (cement, bricks, glass) who face both higher kiln/furnace costs and a construction downturn; or chemical manufacturers reliant on gas feedstock.

Some positive offsets exist, For example, Australian defence-related manufacturing and certain food manufacturers might see stable or higher demand. Overall, however, manufacturing’s risk profile is rising. CreditorWatch’s BRI metrics for manufacturing are likely to tick up, reflecting slower payments and tighter credit terms. Small and medium manufacturers with thin liquidity are the most vulnerable.

Construction

The construction industry had just been through a significant period of stress, with high interest rates and rapid input cost inflation causing widespread closures of building companies post-COVID. In the second half of 2025, insolvencies had tended to level out, albeit still at relatively elevated levels, reflecting lower interest rates through 2025.

Construction is extremely fuel-dependent (earthmoving equipment, generators and transport of materials all rely on diesel) while production of essential materials like cement, bricks, glass and steel is often very energy intensive. The sector failure rate of 5.8% is above the national average and it is ranked second among all industries for payment defaults. This indicates many subcontractors and suppliers to construction are not being paid on time.

The oil price spike will likely increase pressure on construction firms. Some construction companies have clauses to adjust for fuel cost increases, but many smaller ones do not. We expect to see an acceleration of construction company failures across 2026, if prices remain elevated. Recent interest rate increases will also slow demand.

The civil construction segment (infrastructure projects) may fare a bit better as government clients sometimes adjust contract values for cost inflation. However, civil contractors must also manage volatile asphalt and fuel costs.

The only silver lining is that the government is aware of construction’s strategic importance (for housing supply and infrastructure) and may intervene. Already, there’s talk of extending relief on fuel taxes for heavy vehicles and expediting claim payments on government projects to improve contractors’ cash flow. Such measures might cushion some firms.

Ultimately though, construction is in for a tougher period unless oil prices fall soon. This energy shock has struck when the industry has just come out of a pressured time. Stakeholders should brace for more news of builder distress, project delays and a need for careful risk management in any new construction contracts.

Agriculture

Farmers are heavily reliant on diesel fuel for farm machinery, irrigation pumps and transport of produce. They also depend on fertilisers, whose prices track natural gas (the main input to fertiliser) and where around 10% of global supply is reported to transit through the Strait of Hormuz. The price of Urea, the key ingredient in nitrogen fertiliser, is up more than 50% year-on-year. The national average cost of diesel has risen from 180.9c/litre on 1 March to 245.6c/litre on 15 March.

Despite these cost pressures, the failure rate of Agricultural businesses is well below the national average, in part because of a succession of very favourable harvests. If oil prices remain elevated into planting and harvesting seasons, cash flows could deteriorate, potentially increasing rural loan delinquencies later in 2026. On the flip side, if any global food supply issues arise (e.g. Middle East turmoil affecting trade logistics), Australian producers might see higher prices for commodities like wheat or meat, which could partially offset their cost pressures. Overall, however, the initial effect for agriculture is a cost squeeze.

We anticipate a moderate uptick in farm insolvencies from historically low levels if high fuel costs persist beyond the next quarter (many smaller farms have thin buffers). For now, though, agriculture’s risk exposure remains relatively benign – a reflection of low starting leverage and the essential nature of food production, which maintains baseline demand.

Mining

The mining sector presents a mixed picture. On one hand, mining operations (especially metalliferous mining and coal mining) are energy-intensive, consuming vast amounts of diesel for transport and electricity for processing. Higher energy costs raise the cost of production. On the other hand, miners are often sellers of energy or commodities tied to energy.

Indeed, Australia is a major exporter of coal and LNG (liquefied natural gas), whose prices have risen alongside oil. Other metals miners are currently enjoying elevated prices including for copper, gold, uranium and lithium, partly due to safe haven demand and to the strong growth in AI.

Financially, mining companies entered 2026 in solid shape overall. CreditorWatch’s data for February shows mining’s business failure rate was 4.6% for the previous 12 months, roughly the same as Healthcare and below the national average. The insolvency rate in mining (around 1.0% annually) is relatively low as well. This sector saw few insolvencies in 2025, thanks to high commodity earnings.

The Middle East conflict, will provide energy producers with a profit windfall, though other miners like other businesses will experience increased costs. Australian LNG exporters are seeing higher spot gas prices in Asia (as buyers hedge against Middle East supply risk), and thermal coal prices have also ticked up. Meanwhile, Miners of gold and critical minerals enter the crisis with very healthy commodity prices (gold and copper prices near record highs, for example).

However, not all is positive: miners must manage higher operating costs, and those not directly linked to energy (e.g. iron ore) could suffer if a global slowdown reduces industrial demand. At this stage, though, mining is arguably the least at risk of the energy exposed sectors highlighted in this report. Larger miners have hedging programs for fuel and often generate some of their own power on-site, buffering them somewhat from immediate cost spikes. They also hold very healthy cash reserves.

We expect very few mining company failures due to the conflict. If anything, the greater risk would be indirect – for instance, if a global recession hits commodity prices broadly later in 2026.

The outlook

CreditorWatch Chief Economist Ivan Colhoun says, the duration of the conflict and extent of oil price rises are the two key factors impacting Australian businesses.

“A sustained oil price of over US$125-150 per barrel (sustained equals more than three to six months), will seriously pressure consumers’ budgets and business’s costs, and substantially increase the probability of recession.

“The RBA’s February interest rate rise adds to that pressure, though I would expect the Bank’s Board to not raise interest rates again in May, while it seeks to understand the longevity and impacts on the economy from current oil prices.

“The implications for businesses are quite clear. As long as oil prices remain very elevated, there will be increased pressures on many businesses and unfortunately the likelihood is of an increase in insolvencies. There is also the risk that fuel supplies are significantly disrupted throughout the economy, causing a COVID-like shutdown event. The best development would be a very swift end to the conflict and quick reopening of the Strait of Hormuz.”

Business insights

business risk index

Cash Flow

Chief Economist

Credit Management

data

defaults

hospitality

insights

insolvencies

insolvency

Interest Rates

Trump

Head of Media & Communications

Michael joined CreditorWatch in July 2021. He has more than 20 years’ experience in business journalism, marketing and communications strategy, and digital content development. He is passionate about communicating to the business community how CreditorWatch’s products can help them identify risk earlier, and make smarter decisions. He has previously written for Newscorp, Nine publishing, ACP Magazines and the World Economic Forum. He holds Bachelor of Communications and Master of Journalism degrees from the University of Technology, Sydney.

14-Day Free Trial

Get started with CreditorWatch today

Take your credit management to the next level with a 14-day free trial.