CreditorWatch, has released the April results for its Business Risk Index (BRI), revealing both good and bad news for Australian businesses.

Encouragingly, the level of insolvencies has plateaued in recent months, albeit at high levels. Insolvencies in the two hardest hit industry sectors, Construction and Food and Beverage Services, have similarly shown signs of plateauing at high levels, though the significant rise over the past year means a record 1 in 10 hospitality businesses in Australia shut down over the past 12 months.

Two interest rate cuts this year, with the prospect of further reductions in coming months, together with slower price increases and lower fuel prices, are positives for Australian businesses. However, this must be balanced against the uncertainties and impacts of the Trump administration’s tariff policies.

Companies entering insolvency for the first time

Seasonally adjusted

Data sources: CreditorWatch, ASIC, Macrobond

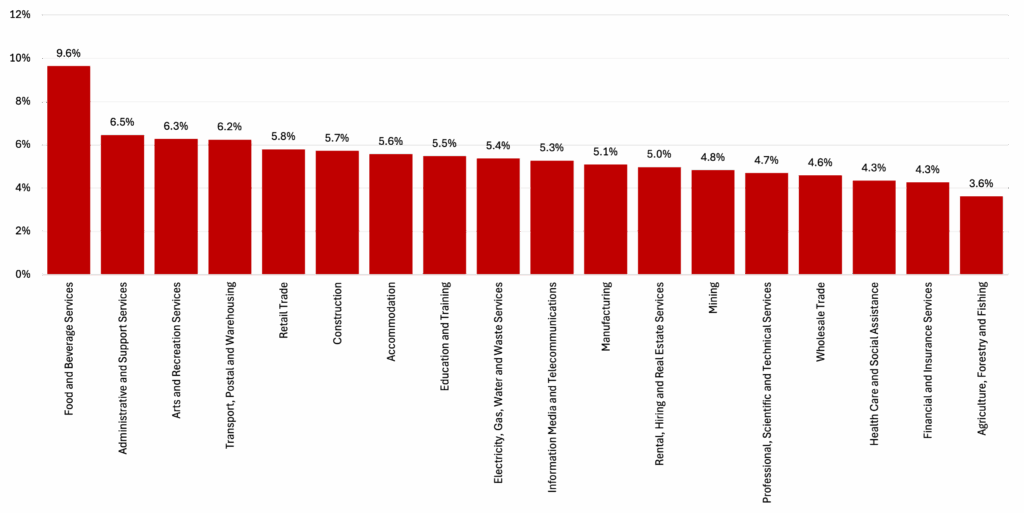

The hospitality sector has been under intense strain, with rising operating costs and weakened consumer demand driven by ongoing cost-of-living pressures leading to 9.6% of businesses in the sector closing their doors in the past 12 months.

The Food and Beverage Services industry not only leads in business closures but also ranks highest across three key indicators of financial distress: insolvency rates, arrears (late payments) and ATO tax debt defaults over $100,000.

Rolling annual business closure rate by industry

12 months to April 2025

Data sources: CreditorWatch, ASIC database direct link

CreditorWatch CEO Patrick Coghlan says hospitality businesses are particularly vulnerable in several key areas.

“First, and most significantly, they are exposed to the vagaries of discretionary spending,” he says. “So, when households feel the pinch from interest rate rises and price increases, they typically spend less at places like cafes, restaurants, bars and pubs. The increase in people working from home has also had an impact, mainly in outlets in CBD areas.

“On top of that you have the business cost increases in areas such as wages, electricity, insurance and food and alcohol.

“You also have to remember that most hospitality outlets are small businesses, so they usually don’t have the cash buffers to get them through hard times that large businesses often do. I really feel for them – it’s tough right now. There are many businesses out there barely hanging on.

“We don’t expect a major turnaround for the sector until households feel the impacts of at least a couple of further rate cuts in their budgets.”

CreditorWatch Chief Economist Ivan Colhoun says, “We hear so much about the cost-of-living crisis, but it’s a ‘cost of doing business crisis’ as well, with businesses having seen significant increases in their cost bases.

“Businesses exposed to discretionary spending experience the worst of both worlds, with their costs pressured and their customers’ demand weakened. Hopefully the recent interest rate cuts by the RBA can build on the beneficial effects of last year’s income tax cuts and cost-of living support.”

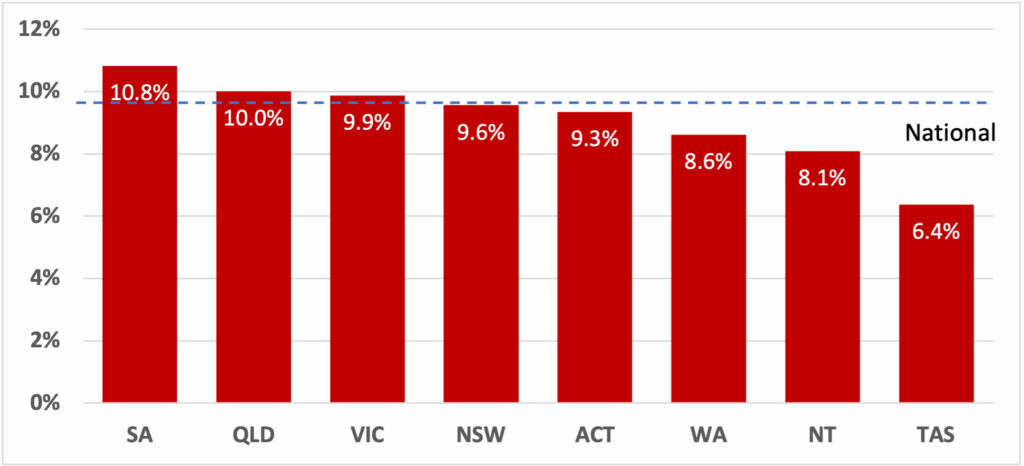

On a state-by-state basis, hospitality businesses in South Australia have been the hardest hit, while businesses in Tasmania have been more resilient than in other states and territories. Both states have seen relatively favourable rates of return to work, with South Australia also recording very strong population growth in recent years.

South Australia is currently recording the lowest level of consumer confidence of any state, while the NAB Survey sees South Australian businesses recording relatively weak business conditions as well.

Hospitality business closure rate by state/territory

12 Months May-24 to April-25

Data Sources: CreditorWatch, ASIC database direct link

INSOLVENCY RATES MODERATE; SIGNS OF IMPROVEMENT IN CONSTRUCTION AND FOOD AND BEVERAGE SECTORS

In a pleasing sign for the Australian economy, overall insolvencies continue to plateau, a trend also in evidence in recent months in both Construction and Food and Beverage Services, the two hardest hit sectors, which combined have accounted for around 40% of all insolvencies over the past year. If sustained in coming months and supported by interest rate cuts, this should arrest the very negative trends for insolvency rates.

Insolvencies – Construction, Accommodation & Food Services

Seasonally adjusted

Data sources: CreditorWatch, Macrobond

B2B PAYMENT DEFAULTS ALSO SHOW SIGNS OF PLATEAUING

CreditorWatch’s proprietary measure of B2B invoice defaults has risen in recent years as costs, interest rates and renewed tax default collections have impacted. Like insolvencies, invoice payment defaults have plateaued in recent months, another encouraging sign ahead of the uncertainties that will flow for businesses globally and in Australia from President Trump’s tariffs and trade war.

B2B payment defaults

Seasonally adjusted, Feb 2020 = 100

Data sources: CreditorWatch, Macrobond

BUT RISING PAYMENT DELAYS INDICATE CASHFLOW PRESSURE PERSISTS

A continuing rise in late payments by companies (rising days past due) supports the RBA’s recent decision to trim interest rates as inflation pressures moderate. Over the past 12 months, Australian businesses recorded payments that were an average of 9.58 days past due.

Days Past Due – Australia

Seasonally adjusted

Data sources: CreditorWatch, Macrobond

ANALYSIS OF HIGHEST AND LOWEST RISK REGIONS

The April results for the Business Risk Index show that the six worst performing regions in Australia are all in Sydney’s west.

As well as experiencing commercial property prices and rents that are well above the national average, these regions have high levels of personal insolvency and lower than average income levels. Businesses in Bringelly-Green Valley in Western Sydney have a forecast average business closure rate of 7.90% over the next 12 months.

The lowest risk region in Australia is Norwood-Payneham-St Peters in inner-city Adelaide. Businesses in that area have a forecast average closure rate of 4.57% over the next 12 months. As well as inner-Adelaide, the lowest risk regions remain concentrated around regional Victoria and North Queensland.

Adelaide has the lowest forecast failure rate among the capital city CBDs (5.20%), followed by Perth (5.30%), Melbourne (5.85%) Brisbane (5.88%) and Sydney (6.25%).

CREDITORWATCH’S OUTLOOK

CreditorWatch Chief Economist Ivan Colhoun says the economy is at particularly interesting crossroads. Insolvencies remain elevated but have not deteriorated in recent months, the previous rising trend likely arrested by the income tax cuts of mid 2024 along with Federal and State government cost of living support measures. It’s too early for the RBA’s February interest rate cut to be influencing these figures, though that cut and this week’s rate reduction will be welcomed by both businesses and consumers. And should have beneficial effects in the second half of the year.

Working against this more favourable setting is likely to be a combination of slower population growth, the effects of continued high costs and the uncertain impacts of President Trump’s tariffs and trade wars globally.

Tariff effects have seen the RBA trim its forecast recovery in GDP growth (from 2.4% to 2.2% over 2025), raise its unemployment forecast very slightly (from 4.2% to 4.3%), and reduce its inflation forecasts to a broadly at target 2.6% throughout the forecast horizon. Importantly, these forecasts are conditioned on around a further two cuts in the cash rate but are made under significant uncertainty as to what the final scope of US tariff policy will be.

Thankfully there has been some unwinding of tariffs in recent weeks, though the net effect on global growth is still expected to be contractionary. Taken together, we expect an elevated level of insolvencies to remain over the next six months.

Subscribe for free

Subscribe for free here to receive the monthly Business Risk Index results in your inbox on the morning of release. No spam.

Business insights

business risk index

Cash Flow

Chief Economist

Credit Management

data

defaults

hospitality

insights

insolvencies

insolvency

Interest Rates

Trump

Head of Media & Communications

Michael joined CreditorWatch in July 2021. He has more than 20 years’ experience in business journalism, marketing and communications strategy, and digital content development. He is passionate about communicating to the business community how CreditorWatch’s products can help them identify risk earlier, and make smarter decisions. He has previously written for Newscorp, Nine publishing, ACP Magazines and the World Economic Forum. He holds Bachelor of Communications and Master of Journalism degrees from the University of Technology, Sydney.

14-Day Free Trial

Get started with CreditorWatch today

Take your credit management to the next level with a 14-day free trial.