SYDNEY, Thursday 13 October – The September 2022 CreditorWatch Business Risk Index (BRI) has revealed the risk of default over the next 12 months has increased in all regions across Australia with 5000 or more registered businesses with the exception of the Lower Hunter and Wyong regions in New South Wales.

From the east coast to west coast, businesses are doing it tough as they battle labour shortages, rising inflation, interest rate rises and supply chain issues.

Key Business Risk Index insights for September:

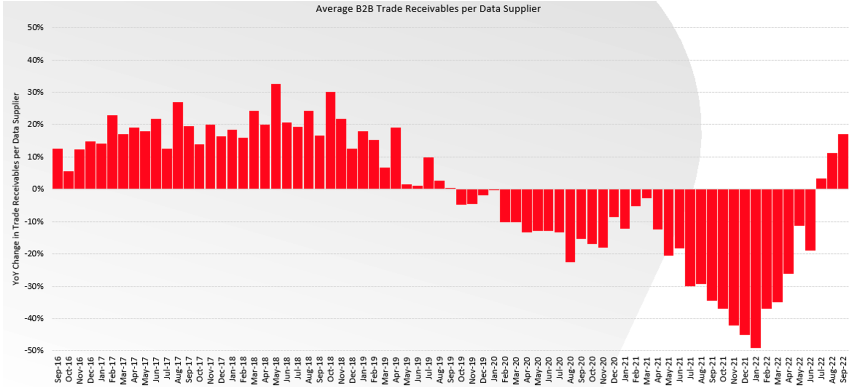

- B2B trade receivables have been steady over the quarter and are up 77% since January.

- YoY growth in B2B trade receivables continues to increase which points to the continued recovery in trade activity for small businesses since Covid.

- External administrations have dropped for the second month in a row following a seasonal pattern. Overall, they remain significantly up from last year and up 42% since January.

- Court actions are up 60 per cent year-on-year.

- The industries with the highest probability of default over the next 12 months are: Food and Beverage Services (7.20%); Arts and Recreation Services (4.68 %); and Education and Training: (4.63 %)

The Top 5 best and worst performing regions across Australia in September:

Click here for additional insights into the top and best performers.

CreditorWatch CEO Patrick Coghlan said B2B trade payment defaults showed a dip this month however, these remain well above levels seen in September last year during Covid, and are a lead indicator of future defaults.

“Payment defaults are hugely significant and are a key indicator of coming delinquency for the debtor/customer. Approximately 25% of businesses with a default end up in administration within 12 months. Additionally, it puts pressure on the supplier who will now have to shoulder that bad debt. A business with a trade payment default are 7 times the default risk compared to a business with a clean payment record.”

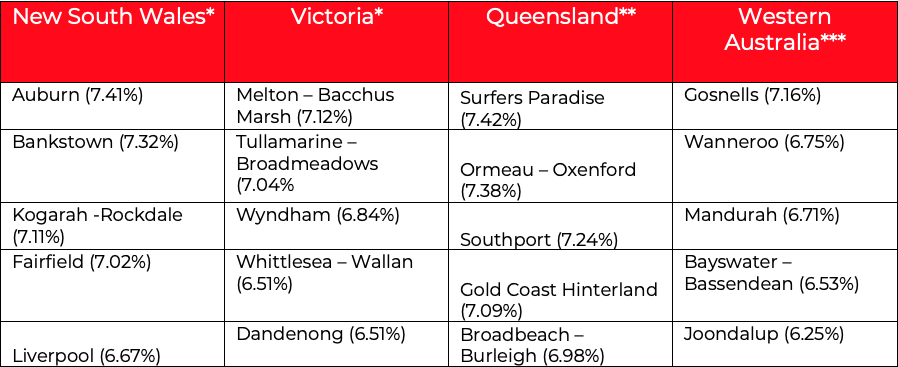

Top 5 regions with highest probability of default over the next 12 months

The BRI also identifies those regions that have the highest and lowest risk of default over the next 12 months.

The top 5 regions by state with the highest probability of default are:

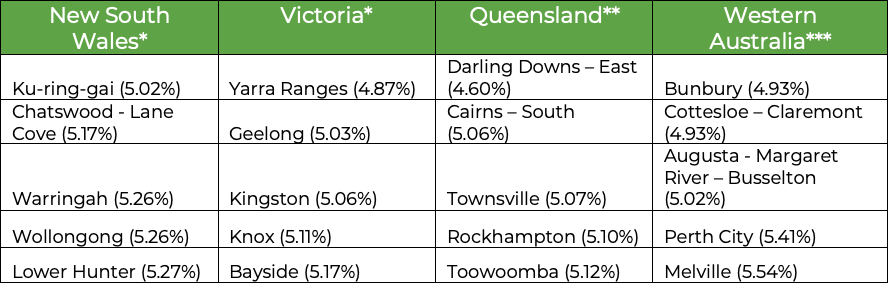

The top 5 regions by state with the lowest probability of default are:

* Regions with more than 5,000 registered businesses

* * Regions with more than 2,500 registered businesses

*** Regions with more than 2,000 registered businesses

A full regional breakdown per state can be found here.

According to CreditorWatch Chief Economist, Anneke Thompson, the September BRI data broadly reflects the conditions of the wider economy, where trade activity is very strong, but medium and longer term risk is heightened. At the moment, Australian businesses are very confident, as evidenced by NABs August Business Sentiment Survey, where conditions now sit +20 index points and confidence sits at +10 index points. However, markets are very reactive to any and all data points, both domestic and global, as businesses and investors try to get a read on what the global economy could look like in 2023. Central banks have been on a warpath against inflation for some months now, and there is growing fear that this could tip some economies in to recession.

Trade activity improves but still down on pre-Covid levels

On a more positive note year on year growth in B2B trade receivables continues to increase which points to a continued recovery in trade activity for small businesses since covid. However figures remain well below pre-covid levels.

Trade activity is returning to more normal levels, however this is after a sustained period of declining activity. The data suggests there are still limits to activity impacting our customers that weren’t there pre-Covid. These limits are likely the lack of or long delay in receiving supplies, particularly in the construction sector, as well as labour shortages preventing expansion or businesses operating at full capacity.

Outlook

While businesses are currently experiencing good demand and trade conditions, economists are now waiting on the full impact of interest rate rises to hit consumers. There are some early signs that business conditions have peaked, both here and globally. Recent ABS Job Vacancy data showed a decline in jobs available in Australia in August compared to May. The data in the US is showing a similar trend. So while labour force data is still very tight in both countries, the vacancy data suggests that jobs are now starting to be filled at a greater rate and businesses have slowed their appetite for employees. It may take some months before this slowdown starts to show up in labour force data, but clearly the RBA are being more cautious in their approach to monetary policy tightening as some indicators start to show that their cash rate hikes are starting to take effect.

-ENDS-